As we witness the gradual unwinding of the rapid growth experienced during the post-pandemic era, it has become evident that property values are struggling to keep up with the Federal Reserve’s swift pace of interest rate hikes. Acquiring suitable investment properties has proven to be quite challenging over the last few months. In response to these new market conditions, Equity Yield Group launched a preferred equity fund approximately eight months ago. Our investment thesis was simple, yet prudent: with prices not adjusting enough to justify new acquisitions, and the investment opportunities presenting more risk than reward, we opted to target placing capital in existing deals in a preferred equity position. This approach helped mitigate risk by subordinating common equity to our investment.

The current economic stress has affected many deals due to higher debt service costs and the prevalent trend of cash-in refinancing. As a result, we anticipated numerous opportunities to deploy rescue capital through this investment strategy. However, despite reviewing several deals, we found zero viable investment opportunities, and instead, encountered numerous distressed deals attempting to delay the inevitable.

Regardless of whether investors are willing to admit it, the signs of a changing market are becoming more apparent. It brings to mind the familiar lyrics of Kenny Rogers: “you got to know when to hold em, know when to fold em, know when to walk away, and know when to run.” And Kenny Rogers may be the opening act before the Fat Lady takes the main stage to announce a commercial real estate crash!

Real estate investors are no strangers to challenges like higher interest rates, debt maturities, expiring interest rate caps, the delivery of new supply, rising operating costs, and inflation eroding consumer budgets.

These risk factors have always been part of real estate investing and are normal contributing factors in the natural progression of real estate and economic cycles. However, what sets this market environment apart is the unnatural progression of the debt cycle driven by the Federal Reserve’s monetary policy.

Preceding their historic velocity of rate hikes, the Fed rapidly cut rates to zero, creating a “free money” environment that gave rise to a bridge debt market. Many investors took advantage of incredibly cheap short-term variable rate loans, leading to overleveraging. The use of bridge debt became self-reinforcing, as investors employing high leverage bid up property prices.

Consequently, investors underwriting without bridge debt had to accept significantly lower yields to enter the market at prevailing prices. This exact phenomenon is one of Warren Buffett’s criticisms of real estate investing. As a value investor, he recognizes that real estate tends to be very accurately priced by the market, making it challenging to find mispriced opportunities. This scenario sets the stage for an impending crash.

The easy money policy not only drove up real estate values but also led investors to purchase properties that have become overvalued and overleveraged in the wake of the Fed’s rate hike cycle. Now, many investors face a challenging environment in which they cannot refinance out of their bridge debt without additional cash infusions, and they cannot make a favorable sale as the higher interest rate environment has effectively reduced the market values of their properties.

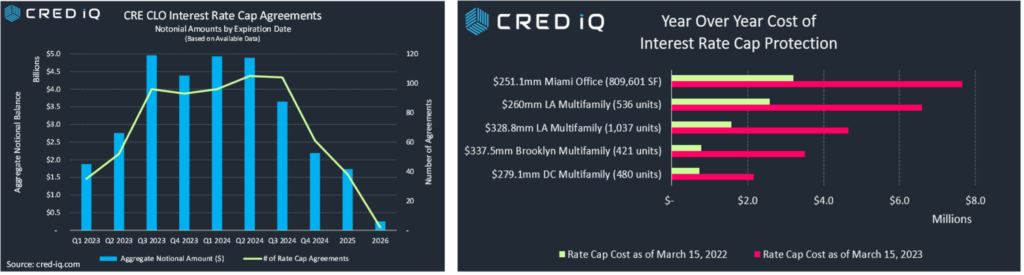

In the last quarter alone, we have seen cap rate expansion of 60bps. The catalyst of expiring interest rate caps and upcoming loan maturities is going to force investors to make some tough choices in the coming months. Q32023 has 120 rate cap agreements expiring, hedging just under $5 billion of bridge debt, and over the next 4 quarters 466 rate cap agreements will expire and $466 billion of commercial mortgages will lose their hedge against interest rates.

The majority of properties cannot support the debt service cost without this interest rate hedge, and the cost of replacing these interest rate caps has more than doubled in the last year alone.

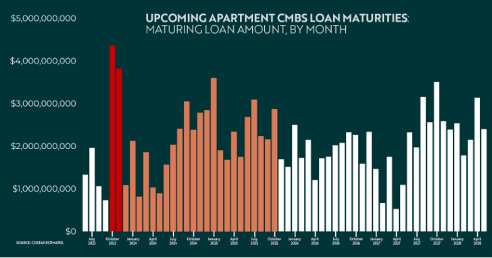

This will require significant recapitalization for many deals. Additionally, the market faces a massive wave of loan maturities in Q42023 with roughly $9 billion of commercial mortgages coming due in October and November.

While many of these deals were purchased at a lower basis before the pandemic boom and may be able to make favorable sales in this environment, all CRE has been devalued by rising interest rates. As a result, a material amount of deals with expiring rate caps and maturing debt are now worth less than the principal balance of their debt.

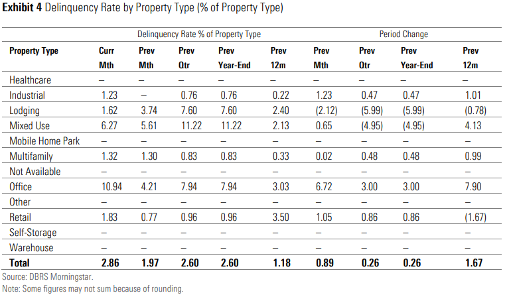

We are now seeing an uptick in mortgage delinquency in CRE CLO pools. As expected, Multifamily and Industrial are posting the lowest delinquency among all real estate types.

Multifamily delinquency has increased almost 1% in the last 12 months and 0.48% in the last quarter. Additionally, lenders seem to recognize the systemic risk of loan maturities, as loan modifications have increased significantly. They now stand at 10% of UPB and special servicing has almost doubled from Q12023 to Q22023. This could be an indication that our fears about CRE mortgage defaults may be just around the corner.

If you would like to learn more about current conditions of the CRE mortgage market, check out the US CRE CLO Quarterly Report.

Distress brings opportunity.

While a looming CRE crash presents a challenge for many owned assets. There will be a rare opportunity to buy commercial real estate at a discount. Given the potential large volume of distressed loans, and distressed sales we could see a moment in which commercial real estate is underpriced, as banks struggle to deal with the logistics of unloading billions of dollars’ worth of real estate.

Although I don’t believe that the coming commercial mortgage crisis will be the catalyst for the Fed to reduce rates I do believe the scale of the problem is larger than the 2008 subprime mortgage crisis. I believe that the next 6-8months will be the beginning of the greatest real estate investment opportunity of the decade. In the words of the great Philosopher Mick Jagger “you can’t always get what you want, but if you try, you might find sometimes, you get what you need.”

As much as we all want rates to come down and property values to return to where they were 12 months ago, what the market needs is a correction, and the strategy of buy high, add value and sell higher only works for so long.

To learn more about how we can help you to generate superior investment results through professionally managed Real Estate investments, click here to register for our investor club.